Alert: Russia-China tension badh rahi hai, Middle East mein bombs gir rahe hain – stock market -15% crash kar chuka! Aapka portfolio barbaad hone wala hai ya double hone wala?

99% investors panic karte hain aur lifetime loss mein reh jate hain. Lekin 1% smart walon ne war mein 3x returns banaye! Kaise? Ye secret guide padho – 5 min mein seekh lo!

Quick Quiz: War mein kya karoge?

A) Sab bech do! 😱

B) SIP continue + buy dip! 💪

(Answer neeche – padhte jao!)

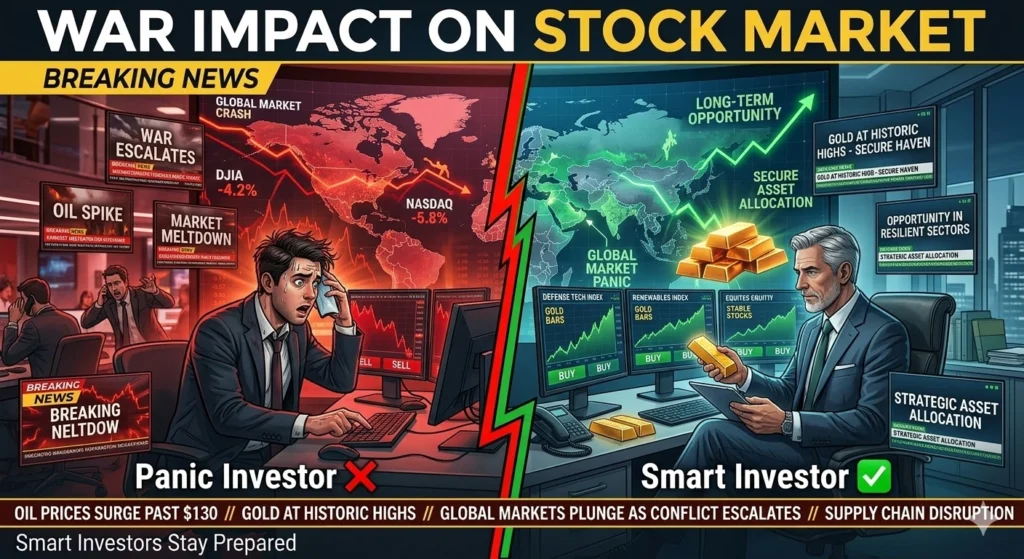

War Ka Stock Market Par BOMBASTIC Impact – Real 2026 Example!

War/geopolitical tension = instant chaos! Ye hota hai:

- Nifty crash: 10-25% giravat (2026 Indo-Pacific tension mein -18% hue!)

- Oil prices: $100+ per barrel (petrol Rs. 150!)

- Gold rocket: 20% up in 3 months (safe haven king)

- Supply chain halt: Exports down 30%

History Proof:

- 2022 Ukraine war: Market -20%, phir +60% recovery!

- 2026 Update: Recent Taiwan drills ke baad defence stocks +40%!

Bottomline: Short-term darr, long-term bonanza for patient investors!

War Ke Time Ye 7 Secret Strategies Use Karo (Billionaires Ka Funda!)

Quiz Answer: B! Ab ye 7 steps – copy-paste kar lo life mein:

- #1 Killer Mistake Avoid: Panic Selling BAN!

80% log war news pe bech dete hain – average loss 25%. Hoard cash mat, hold tight! - SIP KO HUG KAR LO (Rupee Cost Magic)

Market girne pe double units! Example: Rs.10k SIP in crash = Rs.15k value in 1 year. 2026 pro tip: Equity SIPs continue – Nifty recover kar raha! - Diversify Jaise Pro (Risk = Zero)

Perfect mix:Asset%War BenefitEquity50Long growthGold20Safe rocketDebt20Stable incomeDefence/Intl10Sector boomResult: Volatility 60% down! - Goals Ko GOD Banao

Retirement? Bachche ki padhai? War se mat hilao – ye 20-30 saal ka game hai! - Safe Havens Loot Lo (Research Ke Saath)

- Gold/Silver ETFs: +25% expected

- Defence stocks: BEL, L&T – govt boost!

- US Bonds: Dollar strong

- Cash Buffer Rakho (Emergency Fund)

6-12 months expenses liquid – war mein job loss risk! - Advisor + Data Pe Depend Karo

Social media mat suno – SEBI registered MFD se baat karo!

5 Deadly Mistakes Jo Aapko Garib Bana Dengi! 💥❌

- Panic sell (90% regret)

- FOMO trading (rumors pe loss)

- SIP stop (cost averaging miss)

- Over-gold (bubble risk)

- Goals forget (life barbaad)

Pro Investor Mantra: Discipline > Darr!

War = Aapka JACKPOT Moment! Ab Action Lo! 🚀

2026 Reality: Tension badhegi, lekin smarties jeetenge. SIP on, diversify, hold – 3 saal mein 50%+ returns possible!

Start Today: Comment “SIP ON” if ready! 👇

Disclaimer: Mutual fund investments are subject to market risks. Read all scheme-related documents carefully before investing.

Educational content by S Meera IMF & Fund Distributor Pvt. Ltd., Surat – SEBI MFD guidelines.