Retirement planning for working professionals in India has become more important than ever. With rising inflation, increasing life expectancy, and higher healthcare costs, relying only on pensions or savings accounts is no longer enough. Smart professionals start retirement planning early to achieve financial independence, maintain their lifestyle, and secure a stress-free future.

Today, salaried individuals combine EPF, NPS, PPF, and mutual fund investments to build a diversified retirement corpus that grows over time.

Why Retirement Planning Should Start Early

Most working professionals begin retirement planning in their 30s or early 40s, and for good reason. The earlier you start, the more you benefit from the power of compounding, where small, regular investments grow significantly over decades.

Key Reasons to Start Early:

- Inflation reduces purchasing power every year

- Longer investment horizon allows higher equity exposure

- Lower monthly contribution needed compared to late starters

- Ability to handle life events like marriage, children, or career changes

Financial experts often recommend building a retirement corpus worth 25–30 times your annual expenses to live comfortably after retirement.

Key Steps Working Professionals Should Follow for Retirement Planning

1. Set Clear Retirement Goals

Decide:

- Retirement age (usually 55–60 years in India)

- Desired lifestyle (travel, hobbies, family support, philanthropy)

- Expected post-retirement income needs

Clear goals help estimate the exact retirement corpus required.

2. Calculate Future Expenses Accurately

While planning, consider:

- Current living expenses adjusted for 6–7% inflation

- Healthcare costs rising at 10–15% annually

- Lifestyle upgrades post-retirement

Accurate projections prevent shortfall during retirement years.

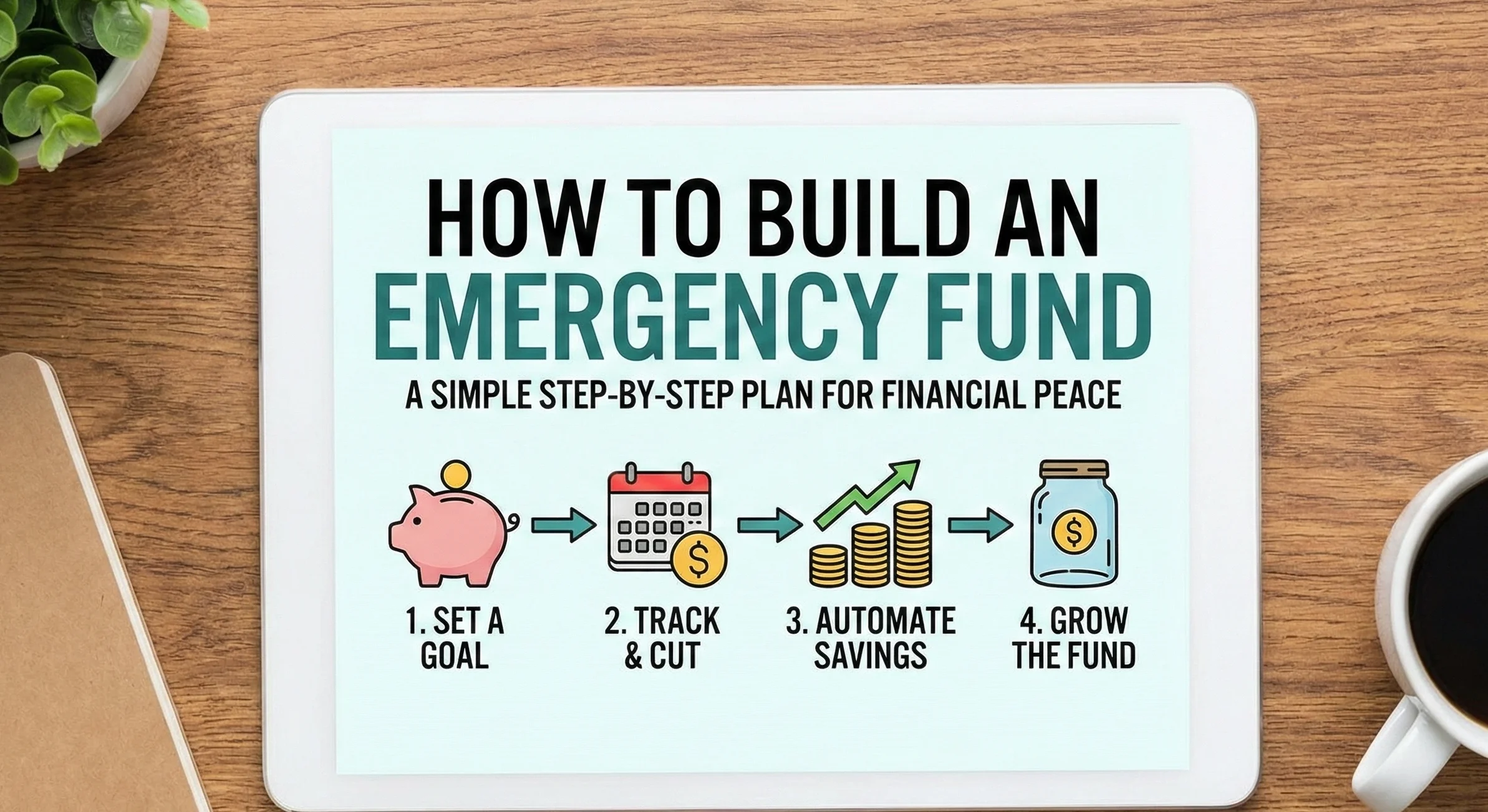

3. Build an Emergency Fund First

Before aggressive investing:

- Save 6–12 months of expenses in liquid funds or savings

- Protect investments from sudden withdrawals

Once done, allocate at least 20% of your monthly salary toward retirement investments using auto-debit SIPs.

4. Review and Rebalance Every Year

Annual reviews help:

- Increase investments with salary hikes

- Adjust asset allocation based on age

- Gradually shift from equity to debt as retirement approaches

This ensures capital protection and stable returns.

Best Retirement Savings & Investment Options in India

| Option | Key Features | Best For | Tax Benefits |

|---|---|---|---|

| EPF (Employee Provident Fund) | 12% employer + employee contribution, stable returns (~8%) | Salaried professionals | EEE tax benefit |

| NPS (National Pension System) | Equity + debt mix, low cost, pension income | Long-term retirement growth | Extra ₹50,000 under 80CCD(1B) |

| PPF (Public Provident Fund) | 15-year lock-in, safe returns (~7.1%) | Conservative investors | Section 80C up to ₹1.5L |

| Mutual Funds (SIP/STP) | Equity for long-term growth (10–12%) | Wealth creation | ELSS tax benefit under 80C |

Younger professionals can take higher equity exposure, while those nearing retirement should prefer debt-oriented instruments.

Common Retirement Strategies Used by Professionals

- STP (Systematic Transfer Plan):

Gradually move money from debt funds to equity to reduce market timing risk. - SWP (Systematic Withdrawal Plan):

Post-retirement, withdraw 4–6% annually to generate regular income without exhausting capital. - Annuity Plans:

Provide guaranteed income for life, suitable for risk-averse retirees. - Debt Funds & Liquid Funds:

Ensure liquidity and stability during retirement years.

Many professionals follow educational content and Hinglish explainers (like those by S Meera IMF) to understand these strategies through real-life examples—breaking myths such as “retirement planning is only for government employees.”

Actionable Retirement Planning Tips for You

- Start with a ₹5,000 monthly SIP in balanced or equity-oriented funds if you’re in your 30s

- Clear high-interest loans early to improve savings capacity

- Increase SIP amount with every salary increment

- Consult certified and experienced financial planners for personalized strategies

Plan Your Retirement with Experts

A well-structured retirement plan ensures dignity, independence, and peace of mind in your golden years.

👉 Get a FREE Retirement Consultation today:

🌐 Visit: https://smeeraenterprise.com

📞 Call / WhatsApp: 9898071863

S Meera IMF & Fund Distributor Pvt. Ltd.

Secure Your Future – Let Experts Handle Your Financial Planning.

Disclaimer

This article is written under MFD (Mutual Fund Distributor) SEBI guidelines. Mutual fund investments are subject to market risks. Past performance is not indicative of future returns.