Budget 2026 ke baad tax-saving options simple aur powerful hain – new regime mein ₹12 lakh tak zero tax! Old regime se ₹1.5 lakh deductions le wealth banao, easy language mein samjhaate hain.

New vs Old Regime – Kaunsa Choose Karein?

New regime mein basic exemption ₹4 lakh, slab 5-30%, aur ₹12L income par full rebate – salaried walon ke liye best. Old regime deductions deta hai jaise 80C, NPS, health insurance – family planners ke liye ideal. Agar deductions ₹2 lakh+ hain toh old better, warna new se tax bachao up to ₹1.14 lakh annually.

Top Tax-Saving Options Post Budget 2026

Yeh options Section 80C (₹1.5L limit), 80D, NPS ke under kaam karte hain, low risk se high growth tak.

ELSS Funds: 3 saal lock-in, equity se 12-15% returns. SIP se shuru karo, mutual funds jaise Parag Parikh Flexi Cap.

Health Insurance (80D): Self/family ₹25K, parents ₹50K deduction.

Home Loan Principal: 80C mein, interest 24(b) alag se.

Kaise Plan Karein Step-by-Step

Income calculate karo, regime choose karo (new default hai).

₹1.5L 80C fill karo: 50% ELSS/NPS, 50% PPF/EPF.

Insurance renew karo, NPS extra daalo.

ITR file karte time proofs attach karo.

Abhi Action Lo!

2026 tax-saving se ₹50K+ bachaao aur invest karo Smeeraenterprise.com par! Free consultation book karo – personalized plan banao: https://smeeraenterprise.com. Start today!

Retirement planning for working professionals in India has become more important than ever. With rising inflation, increasing life expectancy, and higher healthcare costs, relying only on pensions or savings accounts is no longer enough. Smart professionals start retirement planning early to achieve financial independence, maintain their lifestyle, and secure a stress-free future.

Today, salaried individuals combine EPF, NPS, PPF, and mutual fund investments to build a diversified retirement corpus that grows over time.

Why Retirement Planning Should Start Early

Most working professionals begin retirement planning in their 30s or early 40s, and for good reason. The earlier you start, the more you benefit from the power of compounding, where small, regular investments grow significantly over decades.

Younger professionals can take higher equity exposure, while those nearing retirement should prefer debt-oriented instruments.

Common Retirement Strategies Used by Professionals

STP (Systematic Transfer Plan): Gradually move money from debt funds to equity to reduce market timing risk.

SWP (Systematic Withdrawal Plan): Post-retirement, withdraw 4–6% annually to generate regular income without exhausting capital.

Annuity Plans: Provide guaranteed income for life, suitable for risk-averse retirees.

Debt Funds & Liquid Funds: Ensure liquidity and stability during retirement years.

Many professionals follow educational content and Hinglish explainers (like those by S Meera IMF) to understand these strategies through real-life examples—breaking myths such as “retirement planning is only for government employees.”

Actionable Retirement Planning Tips for You

Start with a ₹5,000 monthly SIP in balanced or equity-oriented funds if you’re in your 30s

Clear high-interest loans early to improve savings capacity

Increase SIP amount with every salary increment

Consult certified and experienced financial planners for personalized strategies

Plan Your Retirement with Experts

A well-structured retirement plan ensures dignity, independence, and peace of mind in your golden years.

S Meera IMF & Fund Distributor Pvt. Ltd. Secure Your Future – Let Experts Handle Your Financial Planning.

Disclaimer

This article is written under MFD (Mutual Fund Distributor) SEBI guidelines. Mutual fund investments are subject to market risks. Past performance is not indicative of future returns.

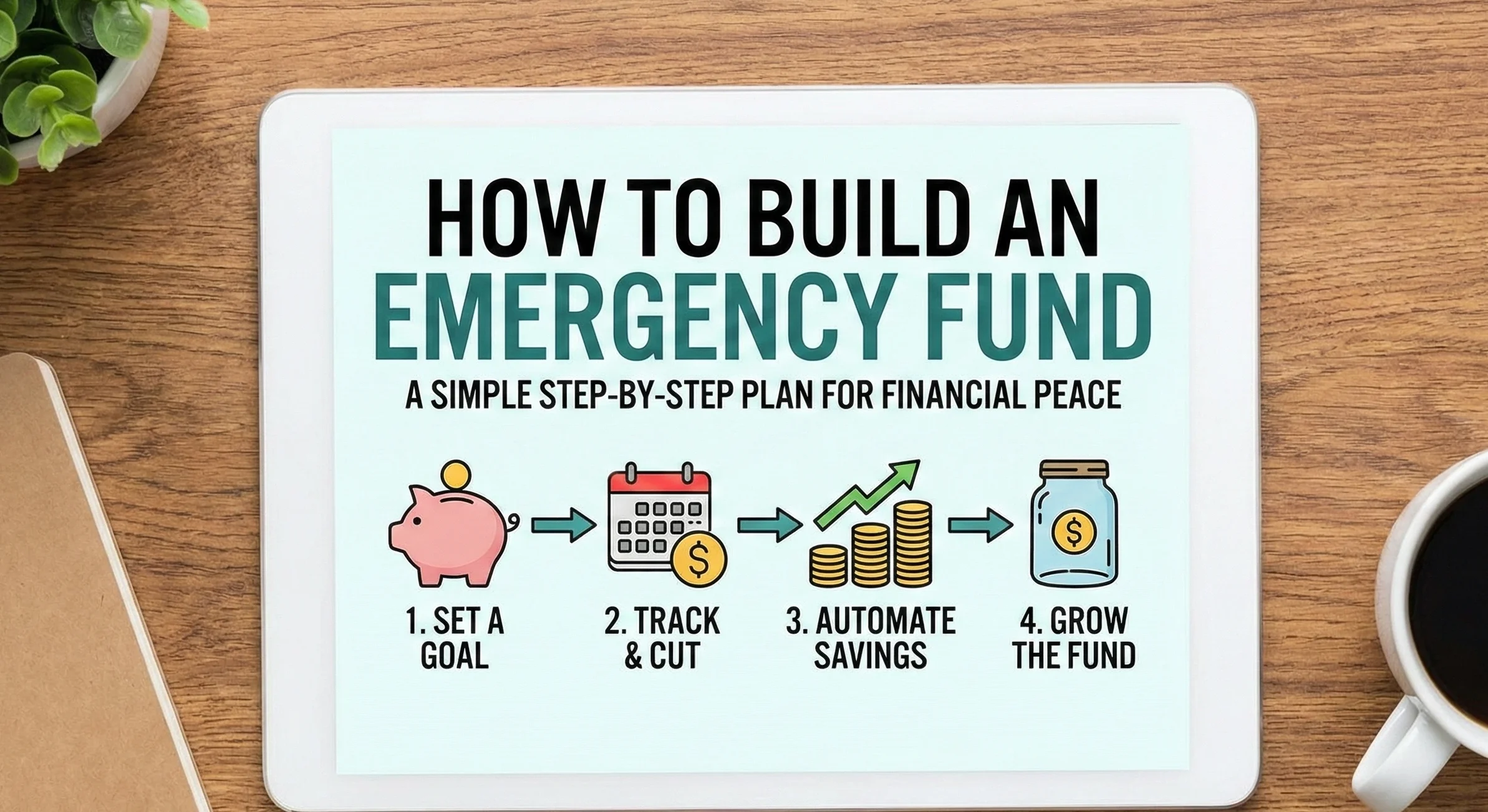

Ever wonder how an emergency fund plays out in the real world? Fast-forward to 2025, where economic shifts, tech glitches, and unexpected twists make financial surprises more common than ever. Inflation’s still lingering, AI is reshaping jobs, and global events like climate changes are hitting wallets hard. But don’t panic—having that safety net can turn “oh no” moments into “I’ve got this.” In this post, we’ll dive into 5 relatable, real-life scenarios based on 2025 trends (drawn from experts like the World Economic Forum and financial forecasts). I’ll keep it simple, fun, and actionable, with tips on how your emergency savings steps in as the hero. Let’s break it down with stories that feel like they could happen to anyone.

Scenario 1: The Tech Job Layoff Wave – When AI Takes Over

Picture this: You’re a marketing whiz at a mid-sized firm, but in 2025, AI tools like ChatGPT upgrades are automating your role. Boom—layoff notice hits. With unemployment hovering at 5-7% (per Fed projections), finding a new gig might take 3-6 months. Without an emergency fund, you’d scramble for loans or dip into retirement savings, adding stress.

How Your Fund Helps: That 3-6 months’ buffer covers rent, groceries, and job search costs (think resume services or networking events). Pro Tip: Use the time to upskill in AI-human collaboration—free courses on Coursera can turn this into a comeback story.45

Scenario 2: Climate Chaos Hits Home – Natural Disasters on the Rise

By 2025, extreme weather events are up 20% (thanks to climate reports), and your coastal home gets flooded from a mega-storm. Insurance might cover some, but deductibles, temporary housing, and repairs could cost $10,000+. If you’re in a high-risk area, this isn’t “if”—it’s “when.”

How Your Fund Helps: Pull from your emergency savings for immediate needs, like hotel stays or emergency repairs, while insurance sorts out the rest. Fun Fact: Apps like FEMA’s disaster aid trackers can help you claim funds faster—your fund buys you breathing room to navigate the chaos.

Scenario 3: Health Scare Surprise – Medical Bills Spike Amid Inflation

Healthcare costs are ballooning in 2025, with average premiums up 8% (per Kaiser Family Foundation). Say you twist an ankle playing weekend soccer—ER visit + follow-ups = $5,000 out-of-pocket. Or a family member needs unexpected surgery. High-deductible plans mean you’re on the hook.

How Your Fund Helps: Cover the gap without maxing credit cards or delaying care. In a pinch, it prevents debt spirals. Bonus: Pair it with a Health Savings Account (HSA) for tax perks—double win for your wallet.

Global trade hiccups from geopolitical tensions (think U.S.-China relations) mean car parts or electronics shortages in 2025. Your car’s transmission fails, and repairs cost 30% more due to delayed imports. Or your fridge dies, and appliances are backordered for months.

How Your Fund Helps: Fund the repair or rental while waiting, avoiding interest on loans. It’s like having a “pause button” on life’s annoyances. Tip: Build your fund with inflation in mind—aim for 4-5% growth in a high-yield account to outpace rising prices.

Scenario 5: Family Life Curveballs – Kids, Weddings, and Unexpected Joy (or Drama)

2025’s family dynamics are evolving: Remote work means more relos, or a surprise wedding for your sibling. But what if a kid’s college fund needs a boost, or a pet emergency vet bill pops up? These “happy” events can strain budgets unexpectedly.

How Your Fund Helps: Handle the extras without derailing your plans. For example, cover a short-term gap in childcare during a move. Remember, it’s not just for disasters—it’s for life’s adventures too!

Why 2025 Makes an Emergency Fund Even More Crucial

With economic uncertainty (recessions possible, per IMF), job volatility from AI, and rising costs, experts say 70% of Americans are underprepared for emergencies. But building one now sets you up for 2025’s twists. Start small: Automate $100/month, cut one subscription, and watch it grow. It’s not boring—it’s empowering.

Final Thought: Life in 2025 will throw surprises, but your emergency fund is your secret weapon. Ready to build yours? Check out our step-by-step guide and share your 2025 worries in the comments—we’ll brainstorm solutions!

Disclaimer: These scenarios are speculative based on 2024 trends; actual events may vary. Consult a financial advisor for personalized advice.

Investing your hard-earned money can seem complicated, especially with new technologies like artificial intelligence (AI) changing how investments are managed. You might hear a lot about AI automation in finance, but which is really the best choice for your money? Let’s explore the differences and why physical investing often remains the best option for most people.

What is Physical Investing?

Physical investing means making investment decisions based on human knowledge, experience, and advice. It involves working with trusted financial advisors, researching companies and mutual funds, and picking investments with a personal touch. This approach has been around for decades and has helped many grow their wealth steadily.

What is AI Automation in Investing?

AI automation uses computers and smart algorithms to analyze data and make investment decisions automatically. Robo-advisors and AI tools can rebalance your portfolio, trade stocks, and suggest investments based on mathematical models. This can be very fast and efficient, handling complex data that humans might struggle with.

Why Physical Investing is Better for Your Money

Personalized Advice: A skilled human advisor understands your unique goals, risk tolerance, and financial situation. They can give you advice tailored just for you.

Experience and Judgment: Humans bring years of experience, intuition, and understanding of market cycles that AI cannot fully replace.

Trust and Transparency: You can talk to your advisor, ask questions, and get clear explanations. AI decisions can feel like a “black box” because they are based on complex algorithms.

Emotions and Ethics: Humans can consider factors like ethics or social impact in investments, while AI only works on data and patterns.

Flexibility: Human advisors can adapt to unexpected changes in your life or market conditions with a flexible approach. AI follows fixed rules and data.

Security: Human-led investing tends to have less risk of hacking or technical failures that may affect AI systems.

When AI Automation Can Help

AI can be a useful tool to support physical investing by providing extra data analysis and automation for simple tasks. However, relying completely on AI without human oversight can be risky due to its complexity and data dependencies.

Conclusion: The Best Choice

While AI automation is exciting and growing fast, physical investing with a trusted advisor is still the best choice for most investors who want personalized, transparent, and flexible financial guidance. The human touch in investing builds confidence, reduces stress, and ultimately helps safeguard and grow your money over the long term.

Ready to start investing the right way?

Partner with experts at Smeera Enterprise who combine proven traditional financial advice with smart tools to guide you every step of the way. Visit smeeraenterprise.com and take the first step toward securing your financial future today!

In 2025, deciding between Mutual Funds and Fixed Deposits (FDs) depends on your financial goals, risk appetite, and investment horizon. Mutual funds, especially equity and balanced funds, generally offer higher returns—often around 10%-15% annually over the long term—because they invest money in a diversified portfolio of stocks and bonds. On the other hand, fixed deposits provide fixed and guaranteed returns, usually between 6% and 7.5% per year, making them suitable for conservative investors seeking safety and stability.

Why Choose Mutual Funds?

Mutual funds can help your money grow faster because their returns depend on market performance. For example, equity mutual funds have historically given better returns than FDs over 5-10 years. Additionally, mutual funds are tax-efficient if held long-term, with capital gains taxed lower than FD interest income. They are also more liquid—allowing you to redeem your investment easily after a lock-in period. However, because they are linked to market risks, the value of your investment can go up or down in the short term.

Why Choose Fixed Deposits?

Fixed deposits are ideal when you want assured returns and your priority is capital protection. They are less risky than mutual funds because your principal and interest are guaranteed by the bank. FDs suit short-term goals or conservative investors who don’t want market fluctuations. The downside is that returns may not keep up with inflation, and FD interest is fully taxable according to your income slab.

Who Should Invest Where?

Invest in Mutual Funds if: You want long-term growth, can tolerate market ups and downs, and aim to beat inflation.

Invest in Fixed Deposits if: You prefer steady returns, want to preserve capital, or have short-term financial needs.

Simple Comparison at a Glance

Aspect

Mutual Funds

Fixed Deposits

Returns

Market-linked, 10%-15% long term

Fixed, 6%-7.5%

Risk

Moderate to high

Low

Taxation

Capital gains tax (lower if long term)

Interest taxed as income

Liquidity

High (after lock-in)

Moderate (penalty on early withdrawal)

Best for

Long-term growth, inflation beating

Capital safety, short-term goals

Final Thought

If you want to build wealth through the power of markets and can handle some risk, mutual funds are the better choice in 2025. But if safety and surety are your priorities, fixed deposits remain a dependable option. Many investors choose to diversify by putting some money in both to balance growth and safety.

Gold is no longer just jewelry or a status symbol — in 2025, it’s one of the most discussed strategic asset classes in the world.

With prices crossing ₹1,22,000 per 10 grams, investors are once again turning to gold not only for its shine but for its portfolio-balancing power.

In this blog, we’ll decode why gold matters, how to invest smartly, and what you should keep in mind in 2025 — all explained under MFD SEBI guidelines.

The 2025 Outlook – Where Does Gold Stand Today?

According to the World Gold Council, gold remains a highly liquid, credit-risk-free asset that retains value over time.

In 2025, India witnessed over 50% growth in gold prices compared to previous years — outperforming equity and debt.

Reports from The Tribune (2025) and Wright Research show that geopolitical uncertainty, inflation, and global rate cuts have all boosted gold’s appeal.

Leading Indian financial experts believe gold will remain a core component of balanced portfolios in the years ahead.

💰 Why Gold Deserves Its Place as an Asset Class

1️⃣ Long-Term Value & Inflation Hedge

Historically, gold has outperformed inflation and provided steady returns during economic uncertainty.

It’s considered a safe-haven asset, meaning it tends to move differently from equities — providing protection during market downturns.

2️⃣ Portfolio Diversification

Gold acts as a “third pillar” in portfolios dominated by equity and debt.

A small allocation (usually 5–10%) can reduce portfolio volatility and improve long-term stability.

3️⃣ Liquidity & Risk-Free Nature

Unlike company stocks or bonds, gold isn’t anyone’s liability — it carries zero credit risk.

With the rise of digital gold, gold ETFs, and gold mutual funds, investing has become easier and more transparent for retail investors.

🪙 How to Invest in Gold in 2025

Here are the most popular ways to invest in gold today:

Investment Type

Features

Pros

Cons

Physical Gold (Jewelry, Bars)

Tangible and traditional

Emotionally valued

Making charges, purity & storage issues

Gold ETFs / Mutual Funds

Traded digitally like shares

Highly liquid, transparent, SEBI-regulated

Requires demat or MF account

Digital Gold (Fractional Investing)

Start from ₹100

Easy, 24×7 accessibility

Not regulated like mutual funds yet

Sovereign Gold Bonds (SGBs)

Govt-backed, earns interest

Tax benefits if held till maturity

Lock-in period applies

Always assess risk, taxation, and liquidity before investing. Consult your financial advisor.

⚖️ Benefits & Limitations of Gold Investments

✅ Advantages

Acts as a hedge against inflation and currency depreciation

Performs well during economic or geopolitical crises

Enhances portfolio diversification and stability

❌ Limitations

Gold does not generate income (no dividends or interest)

Prices can be volatile — timing your entry matters

Physical gold involves making charges and storage costs

🕒 2025 Trend Watch – Should You Buy Now?

Gold prices have already surged over 50% in 2025, touching record highs.

If you already hold significant gold exposure, consider rebalancing rather than over-buying at peaks.

For those with minimal gold exposure (below 5%), starting a small SIP in gold mutual funds or ETFs may be wise.

Focus on asset allocation, not market timing.

Experts suggest a balanced portfolio — combining equity, debt, and gold — performs best over the long term.

Gold continues to shine bright in 2025, emerging as one of the most trusted and profitable investment options for Indian investors. With global inflation, economic uncertainty, and currency fluctuations, gold has once again proved its strength as a safe-haven and wealth-preserving asset.

If you’re thinking about whether gold is still a good buy, this blog explains the latest gold price trends, benefits, ideal portfolio allocation, and the best ways to invest in gold in 2025.

SEO Keywords: gold investment 2025, gold price in India, best gold investment options, gold portfolio allocation, digital gold India, gold ETF 2025, gold returns 2025

💰 Gold Price Trend in 2025

In 2025, gold prices have reached record highs, reflecting strong investor demand and macro-economic pressures.

24 Carat Gold: around ₹12,100 per gram (≈ ₹1,21,000 per 10 grams)

22 Carat Gold: around ₹11,100 per gram

Gold has delivered over 25% returns year-to-date, making it one of the top-performing assets of 2025.

Keywords: gold price in India, gold price trend 2025, 24 carat gold price, gold rate India, gold returns 2025

🌎 Why Gold Is Rising in 2025

The consistent rise in gold prices throughout 2025 is driven by multiple factors affecting both global and domestic markets.

Top Reasons Behind Rising Gold Prices:

Inflation protection: Gold retains value when the cost of living increases.

Currency weakness: A falling rupee makes gold costlier in India.

Geopolitical tensions: Investors move toward gold during global uncertainty.

Central bank buying: Countries like India and China have increased gold reserves.

SEO Keywords: why gold price is increasing, gold investment trend 2025, reasons for gold price rise, gold forecast 2025

💡 How Much Gold Should Be in Your Portfolio?

Experts recommend that investors keep 5% to 15% of their total investment portfolio in gold, depending on risk tolerance and investment goals.

✅ Ideal Portfolio Strategy

Investor Type

Recommended Gold Allocation

Reason

Aggressive (High-risk)

5%

Focus on equities, use gold only as a hedge

Moderate / Balanced

10%

Combine growth with stability

Conservative / Retired

15%

Protect capital and maintain steady value

Example: If your investment portfolio is ₹50 lakh, keeping ₹5 lakh (10%) in gold offers diversification and stability. That equals roughly 41 grams of 24-carat gold at current rates.

Keywords: gold portfolio allocation, how much gold to invest, gold diversification strategy, gold percentage in portfolio

🪙 Best Gold Investment Options in India 2025

Investing in gold is now easier and more flexible than ever before. Here are the best gold investment options in India for 2025:

Digital Gold:

Buy gold online through trusted apps.

Stored safely by gold vaults.

Great for small investors and beginners.

Gold ETFs (Exchange-Traded Funds):

Trade on NSE/BSE like stocks.

Transparent pricing and no storage hassle.

Ideal for long-term wealth creation.

Sovereign Gold Bonds (SGBs):

Government-backed, offering 2.5% annual interest plus gold price appreciation.

No making charges or storage cost.

Physical Gold (Coins, Bars, Jewellery):

Traditional and tangible but includes making charges and purity risks.

SEO Keywords: best gold investment options India, digital gold India, gold ETF 2025, sovereign gold bonds 2025, how to invest in gold

📊 Gold vs Stock Market – Which Performs Better in 2025?

While the stock market has seen fluctuations, gold has delivered steady double-digit returns in 2025.

If you had invested ₹1 lakh in gold at the start of the year, your investment would now be worth around ₹1.25 lakh. Equity markets, in contrast, have shown mixed results.

A balanced approach — combining equities for growth and gold for safety — remains the best investment strategy in 2025.

SEO Keywords: gold vs stock market 2025, gold returns 2025, gold vs mutual funds, gold vs equity performance

🔮 Future Outlook – Gold Investment Beyond 2025

Analysts predict that gold could reach ₹75,000 per 10 grams by mid-2026 if global uncertainty continues.

Key Drivers to Watch:

Inflation and currency trends

Central bank gold purchases

Global interest rate policies

Retail demand for digital gold and ETFs

Experts recommend systematic gold investing (SIPs in gold ETFs or SGBs) to average out prices and build wealth over time.

GIFT City (Gujarat International Finance Tec-City) is India’s first International Financial Services Centre (IFSC) — a world-class financial hub built to connect India’s markets with global investors.

Think of it as India’s own Singapore or Dubai DIFC, where international banks, funds, and financial institutions can set up operations under global-grade regulations, low taxes, and smooth capital movement.

For foreign investors, GIFT City IFSC has opened a new, convenient, and regulated way to invest directly in India — without the old-style restrictions and paperwork.

🏦 Why GIFT City Matters for Foreign Investors

India is one of the fastest-growing economies, offering opportunities in equities, debt, infrastructure, private equity, and fintech. Until recently, foreign investors had to route their investments through offshore entities like Mauritius or Singapore, which involved complex structures and tax confusion.

Now, GIFT City IFSC makes the process much simpler. It’s a one-stop platform that allows global investors to invest, trade, and manage funds under a unified, transparent, and tax-efficient framework.

🌍 Key Advantages of Investing Through GIFT City IFSC

Tax Benefits

Foreign investors get attractive tax incentives:

No capital gains tax on derivatives and certain securities

No GST on financial transactions

No dividend distribution tax

100% tax exemption for up to 10 years in a 15-year period for eligible funds

These benefits make GIFT City one of the most cost-efficient financial centers in Asia.

Global Investment Freedom

From GIFT City, investors can:

Invest in Indian equities, debt instruments, and government securities

Participate in Alternative Investment Funds (AIFs) and mutual funds registered in IFSC

Access offshore investments through India-based fund managers

All this is regulated by IFSCA (International Financial Services Centres Authority), ensuring international-level compliance and investor protection.

Ease of Doing Business

Setting up an investment vehicle in GIFT City is fast and digital:

Simplified approval process

Unified regulatory authority (IFSCA)

Dedicated banking, custodial, and clearing services

Full capital account convertibility for foreign investors

It’s built to make cross-border investing smooth and compliant.

USD-Denominated Ecosystem

All transactions in GIFT City IFSC happen in foreign currencies like USD, not INR. This gives investors full freedom to repatriate funds and avoid foreign exchange risks.

🧭 How Foreign Investors Can Start

Here’s how foreign investors can invest in India through GIFT City IFSC:

Set up or invest in an IFSC-registered fund or AMC

Many Indian and global AMCs already have fund operations in GIFT City.

Register with IFSCA as an FPI (Foreign Portfolio Investor) or partner with an existing fund.

Open an account with an IFSC-approved bank or broker.

Invest in regulated instruments like Indian equities, bonds, or AIFs through the GIFT City platform.

Everything — from onboarding to reporting — is managed digitally and under SEBI-aligned guidelines.

📊 Example: Alternative Investment Funds (AIFs) in GIFT City

Many global investors prefer to invest through AIFs set up in GIFT City, as these funds:

Can raise capital from both Indian and foreign investors

Invest across sectors — equity, infrastructure, startups, and real estate

Offer global-standard fund management and reporting

This structure gives foreign investors diversified exposure to India with strong governance and flexibility.

🚀 Why GIFT City Is the Future of Global Investing in India

GIFT City bridges the gap between India’s domestic markets and international capital. It offers: ✅ Tax efficiency ✅ Regulatory transparency ✅ Seamless fund flow ✅ World-class infrastructure

For global investors seeking to participate in India’s growth story, GIFT City IFSC is the smartest entry point.

For years, Indian investors have had two popular investment choices — Mutual Funds and Portfolio Management Services (PMS). Mutual funds are simple and accessible but often feel too broad or generic. PMS, on the other hand, offers personalized strategies but comes with a heavy price tag — usually ₹50 lakh or more to start.

So what about investors who want something smarter than mutual funds but not as expensive as PMS?

That’s where Specialised Investment Funds (SIFs) are changing the game.

Think of SIFs as the perfect balance between mutual funds and PMS.

They’re professionally managed and SEBI-regulated, giving you more focused investment strategies — all while keeping things transparent and affordable.

You can start investing in SIFs with just ₹10 lakh, making them accessible for serious investors who want professional management without the big PMS entry cost.

👉 In short:

Mutual Funds = Broad and basic

PMS = Personalized but pricey

SIFs = Smart, flexible, and affordable

🔍 Why SIFs Are Gaining Popularity in 2025

Lower Entry Barrier

Earlier, only wealthy investors could access professional-grade management through PMS. Now, with SIFs, you can start with just ₹10 lakh and still enjoy high-quality fund management.

Active and Flexible Strategy

Unlike mutual funds, SIF managers are not tied to tracking an index. They can move across equity, debt, REITs, InvITs, private equity, or derivatives — depending on where the opportunities are.

That means your money works smarter, not just harder.

Strong SEBI Regulation

Every SIF operates under strict SEBI guidelines to protect investors.

No fund can invest more than 10% in a single stock.

Debt exposure per issuer is capped at 20%.

Derivative usage is within defined limits.

You get flexibility with discipline — the best of both worlds.

Tax Benefits Stay the Same

SIFs follow the same taxation rules as mutual funds, which means you don’t lose any tax efficiency even though you get more flexibility.

All-in-One Investment Experience with FYERS

At FYERS, you can explore, compare, and invest in SIFs right from your existing account — no extra paperwork or separate portals. Everything, from fund performance to holdings, is visible in one place.

👥 Who Should Consider SIFs?

SIFs are ideal for investors who: ✅ Already invest in mutual funds but want more control ✅ Have at least ₹10 lakh to invest ✅ Want professional fund management without PMS-level commitment ✅ Are open to active strategies that adapt to the market

However, if you’re a beginner or prefer a “set and forget” style of investing, it’s better to start with regular mutual funds first.

The Future of Smart Investing

SIFs are not just a trend — they’re a new investment category that bridges the gap between simplicity and sophistication.

They offer:

Active decision-making

Transparency

Professional management

Lower minimum investment

All this makes SIFs India’s favorite investment choice for 2025 — especially for investors who want to grow faster but stay safe under SEBI’s framework.

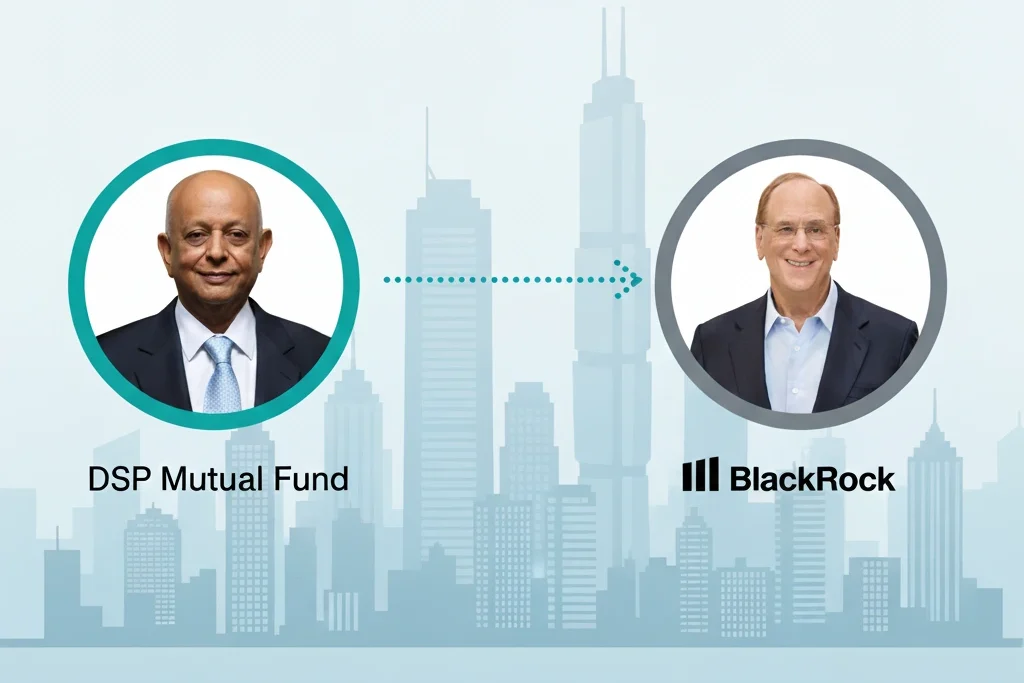

Is Jio BlackRock Mutual Fund Safe? Your Easy Guide (Expert Check)

A Complete 2025 Guide with SEBI Approval, Launch Details & Expert Insight

About the Past of BlackRock Mutual Fund :

The partnership between Jio Financial Services Ltd. (part of the Reliance Group) and BlackRock Inc. (the world’s largest asset manager, managing over USD 11 trillion) marks the launch of a new mutual fund house in India — Jio BlackRock Mutual Fund.

It aims to bring together Jio’s digital reach and BlackRock’s global investing experience to make mutual-fund investing more accessible, transparent, and technology-driven for Indian investors.

As an investor, your first question is natural —

“Is my money safe?”

Let’s answer that clearly.

1. Is Jio BlackRock a Safe Company for Investors?

(Safety from Fraud & Corporate Risk)

Yes — the company itself is safe and well-regulated.

Here’s why:

Strong Ownership: Backed by two credible giants — Reliance (Jio Financial Services) and BlackRock.

Regulation: Jio BlackRock Mutual Fund is governed by the Securities and Exchange Board of India (SEBI) and registered under the Association of Mutual Funds in India (AMFI).

Investor Protection: All mutual funds operate through a trust structure. Investor money is held by an independent trustee and custodian — separate from the company’s own assets.

✅ Meaning: Your investment is protected from fraud and corporate liabilities of the fund house.

However, remember: market risk still exists.

2. Is My Money Guaranteed to Grow?

(Understanding Market Risk)

No. Like all mutual funds, returns are market-linked, not guaranteed.

Your safety and returns depend on the fund category you choose 👇

Fund Type

Example Scheme

Investment Goal

General Risk Level

Best For

Debt / Money Market

Jio BlackRock Liquid Fund

Short-term stability, liquidity

Low

Parking emergency funds (6–12 months)

Equity (Stock Market)

Jio BlackRock Flexi Cap Fund

Long-term growth (5+ years)

High

Wealth building for long-term goals

✅ If you seek safety: Opt for Debt Funds like Liquid or Overnight Funds. ✅ If you seek growth: Consider Equity Funds such as Flexi Cap or Large Cap schemes —but be ready for short-term fluctuations.

3. What Makes Jio BlackRock Mutual Fund Different?

The unique edge is technology and data-driven investment management.

Its equity schemes (such as the Flexi Cap Fund) use a proprietary method called Systematic Active Equity (SAE), powered by BlackRock’s AI-based Aladdin Platform — the same risk management system used globally by institutional investors.

How it works:

AI analyzes thousands of market data points daily.

Helps fund managers make data-backed decisions.

Reduces human bias and supports systematic risk control.

👉 This AI integration may help Jio BlackRock funds respond faster to market changes — a modern advantage for investors.

4. Should You Invest Now or Wait?

(Expert Perspective for 2025 Investors)

Jio BlackRock Mutual Fund is a new asset management company (launched in 2025).

That means:

There is no track record yet of performance across market cycles.

Investors should monitor how its funds perform over time before committing large amounts.

Expert Suggestions:

🟢 Start with SIP: Begin with a small Systematic Investment Plan to test the fund’s consistency.

🕰️ Wait for 3 Years: Allow the AMC to build a track record through different market phases.

💼 Diversify: Use Jio BlackRock for a portion of your portfolio — not the entire investment.

📋 5. Final Investor Checklist

Goal

Suitable Fund Type

Suggested Strategy

Preserve capital

Liquid / Overnight Fund

Short-term investment (3–12 months)

Build wealth

Equity Flexi Cap Fund

Long-term SIP (5+ years)

Balanced returns

Hybrid Fund (Equity + Debt)

3–5 year investment horizon

✅ Always match the fund to your goal. ✅ Focus on time in the market, not timing the market. ✅ Review fund performance annually and rebalance when needed.

📈 Conclusion: Safe Fund House, Market-Based Returns

The Jio BlackRock Mutual Fund venture is backed by two credible institutions and regulated by SEBI, making it a safe fund house from a compliance perspective.

However, like any mutual fund, investment returns depend on market performance and fund strategy — not brand names.

If you believe in long-term investing and value technology-driven fund management, Jio BlackRock could be a promising option to consider in 2025 and beyond.

📢 Final Tip: Invest gradually, diversify wisely, and stay focused on your goals — not the hype.

✅ Quick Fact Summary

Factor

Detail

Company Type

Joint Venture of Reliance Jio Financial Services & BlackRock Inc.

Regulator

SEBI – Securities and Exchange Board of India

Launch Year

2025

Investor Protection

Assets held by independent trustee & custodian

Technology Used

AI-driven Systematic Active Equity (SAE) via BlackRock Aladdin

Safety Level

High corporate credibility + SEBI oversight

Return Nature

Market-linked, not guaranteed

Best For

Digital first-time investors & long-term SIP investors